The FIRE Two-Account Trick: Spend Guilt-Free, Save More

Separate spend from save and saving becomes the default. The peer-reviewed science behind the two-account trick, plus the 4 failure modes that break it.

Want guilt-free spending? Stop mixing your money.

Here is what this looks like in real life:

You get paid $3,000.

Automatically: $600 goes to “FIRE SAVINGS.”

The remaining $2,400 is your bills + your “SAFE TO SPEND” money. If the spend account says $120 for the week, you can spend it without second-guessing.

That is the two-account trick: separate “spend” from “save” so saving happens by default and spending has a clear boundary.

Most articles about budgeting with multiple accounts (like Experian’s overview) stop at the mechanics. This one goes one level deeper: the peer-reviewed behavioral evidence for why partitioning works, and the four failure modes that quietly break the system.

Educational note: this is general education, not financial advice. Results vary. Adapt the numbers to your situation.

Why mixing your money makes spending harder

A single mixed account creates three problems:

1) Every purchase becomes a willpower decision

You are forced to decide, over and over, whether a purchase conflicts with your long-term goal. That is decision fatigue, and it is why even motivated people slip — the same reason most habits fail after 30 days: they depend on daily willpower instead of structure.

2) The big balance is misleading

A big checking balance is not “available to spend.” It includes rent, utilities, next week’s groceries, and your future savings. But your brain sees one number and treats it like permission.

3) Guilt ruins consistency

If you are never sure what is safe, spending feels like failure. And when FIRE starts to feel like constant restriction, people rebel. They abandon the plan, then promise to restart next month, then repeat.

The fix is not stricter rules. The fix is clearer boundaries.

The behavioral science behind the two-account trick

The two-account trick is not just a budgeting hack. It maps to well-studied behavioral mechanisms: mental budgeting, partitioning, and commitment through automation.

Mental budgets actually change behavior

Research on mental budgeting shows that people treat category budgets like real limits, and spending tends to slow when a category feels depleted. A spending account is not just administrative — it changes behavior by making the “limit” feel concrete. (Heath and Soll, 1996, Journal of Consumer Research)

Partitioning money makes it harder to raid savings

In field evidence on earmarking and partitioning, saving increased when earmarked money was partitioned into separate containers rather than pooled, which the authors link to reduced temptation and stronger self-control. (Soman and Cheema, 2011, Journal of Marketing Research)

Automation and pre-commitment increase saving rates over time

The Save More Tomorrow program is classic evidence that when people pre-commit and automate saving increases, saving rates can rise substantially over time. You do not need an employer plan to use the lever: automatic transfers between accounts create a default where saving happens before spending expands. (Thaler and Benartzi, 2004, Journal of Political Economy)

Commitment features can help people accumulate

Randomized evidence from a commitment savings product in the Philippines shows that giving people ways to restrict access to savings can increase accumulation for many users. You do not need to lock money away permanently, but you can add just enough friction that savings is not treated like a second checking account. (Ashraf, Karlan and Yin, 2006, Quarterly Journal of Economics)

Dividing “real” accounts can improve financial well-being

A behavioral chapter focused on partitioning real accounts argues and tests that dividing money into separate accounts can support self-control and financial well-being, aligning closely with a spend vs save setup. (Loewenstein, Cryder, Benartzi and Previtero, 2012)

Put simply: separate accounts reduce temptation, reduce decision fatigue, and make saving the default.

The Two-Account Setup: Spend vs Save

Here is the simplest version:

Account 1: Spend account (safe-to-spend)

This is the account your card uses day to day:

- groceries

- gas/transport

- eating out

- fun money

- small irregular expenses

Rule: if the money is not in the spend account, it is not available.

This is what makes spending feel free: you are spending from a pre-approved sandbox, not negotiating with your entire financial future.

Account 2: Save account (do not casually touch)

This is where your automatic savings lands:

- emergency fund contributions

- investing contributions (if your brokerage pulls from here — and if you are unsure where those contributions should go first, start with the debt-vs-invest decision tree)

- sinking funds (if you use sub-buckets)

Rule: transfers out of this account require intention, not a swipe.

Common routing options (pick one)

Use the one that is easiest to keep consistent:

- Save account → brokerage: paycheck lands, transfer to save, then brokerage auto-pulls monthly from the save account.

- Direct paycheck split: employer sends part of your paycheck directly to savings/brokerage (if offered), remainder to spend.

- Brokerage direct pull from checking: workable, but it can feel “invisible.” If you struggle with impulse spending, “save first, spend second” is usually clearer.

Transfer timing matters: set the save transfer for payday (or the next morning) so spending expands into what is left, not into what you hoped to save.

How to set your numbers without feeling restricted

The most common mistake is setting the spend account too low. That creates scarcity, guilt, and rebellion. The goal is a sustainable system, not a punishment.

Step 1: Look back 2–3 months

Estimate:

- fixed costs (rent, utilities, insurance, debt minimums)

- variable essentials (groceries, transport)

- discretionary (eating out, shopping, entertainment)

You are not judging yourself. You are collecting data.

Step 2: Fund fixed costs first

If fixed costs come from the spend account, make sure they are covered automatically and not competing with your fun spending.

If you want the cleanest version later, you can add a bills account. But for FIRE beginners who want consistency, start with two accounts and keep it simple.

Step 3: Choose a repeatable savings transfer

Pick a transfer you can hit on your average month, not your perfect month. Consistency beats intensity — that is the difference between habits that move the math and habits that just sound smart.

Step 4: Add a small cushion to prevent overdrafts

Fragmentation can increase overdraft risk if you cut things too close. Keep a buffer in the spend account so one surprise charge does not break the system.

A simple starting point: about one week of typical variable spending.

Automate it like a default, not a goal

The two-account trick gets its power when you remove the “should I transfer this month?” debate.

Transfer right after payday

Set the transfer for the same day you get paid, or the next morning.

If income is irregular (founders, freelancers), use percentage transfers

Options:

- transfer a fixed percentage of each deposit, or

- transfer a small fixed amount weekly

For founders, the percentage version is usually the only one that survives lumpy months — the structure stays constant while the dollars flex. (If you are using this system to build runway toward quitting, know the real MRR number you need before leaving your job.)

Increase your savings rate gradually

Borrow the Save More Tomorrow idea: increase savings in small steps.

- Increase your transfer by 1 percent of take-home every 2–3 months, or

- Increase by a fixed amount after each raise

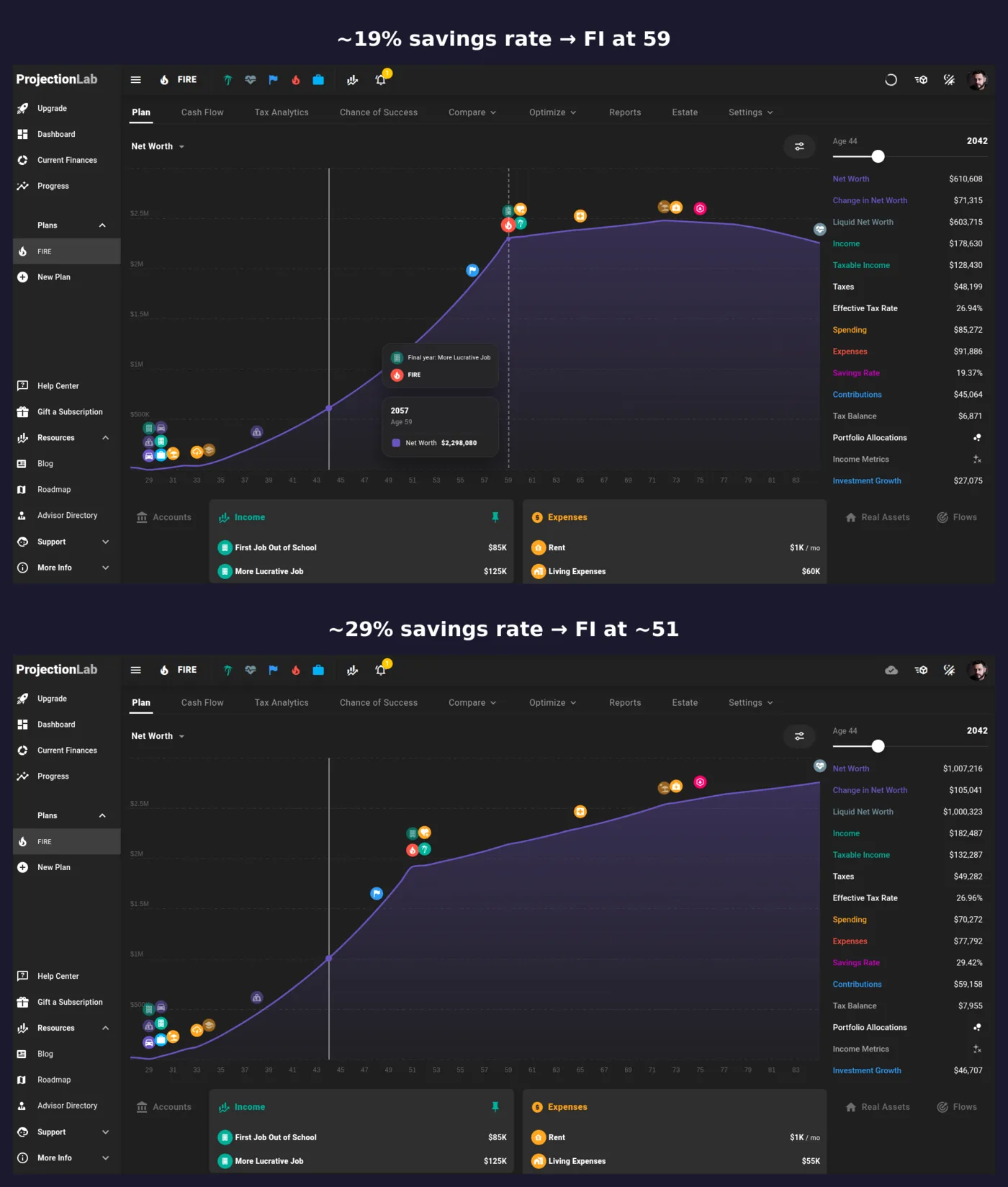

We tested the spread in ProjectionLab’s sandbox: at a roughly 19% savings rate the plan reaches FI at age 59 (2057); raising the rate to about 29% pulls FI forward to around age 51. Same income, same assumptions — the only variable that moved was the savings rate, which is exactly the number the two-account structure exists to protect.

Common failure modes and quick fixes

Failure mode 1: “I overspend because it feels licensed”

Mental accounts can backfire if “fun money” turns into “spend it all.”

Fix:

- Set the spending transfer based on your actual history.

- Add a buffer to avoid a binge-restrict cycle.

- Review monthly and adjust if you hit zero early most months.

Failure mode 2: Fees, minimums, and too many accounts

If you pay fees or juggle too many accounts, friction can outweigh the benefit.

Fix: use a no-fee setup and confirm these basics:

- $0 monthly fee

- no minimum balance requirement

- free ACH transfers

- overdraft fee off (or overdraft protection configured safely)

Failure mode 3: “I do not have surplus to save”

A two-account setup does not create money from nothing.

Fix:

- Treat this as a system for people who can save something, even a small amount.

- If there is no margin yet, focus first on creating it (reduce one fixed cost, negotiate one bill, increase income).

- Once you have margin, this system helps you keep it.

Failure mode 4: Lumpy expenses blow up the spend account

Annual fees, car repairs, gifts, and travel can wreck a clean setup.

Fix:

- Create a mini sinking fund inside the save account.

- Contribute monthly for known lumpy categories.

- Pay those expenses intentionally from the sinking fund instead of draining long-term savings.

A simple 10-minute checklist to start today

1) Open or label two accounts

- Spend account: SAFE TO SPEND

- Save account: FIRE SAVINGS

Labels matter. They make the boundary feel real.

2) Pick a transfer rule

Choose one:

- fixed amount per paycheck

- percentage per paycheck

- weekly fixed amount

Then schedule it right after payday.

3) Add friction (but keep emergencies accessible)

Add one small friction:

- no debit card on the save account

- keep savings at a different bank

- disable instant transfers if you are tempted

Safety note: keep your emergency cash accessible. Friction is for impulse spending, not real emergencies.

4) Turn on alerts

Set alerts for:

- low balance on spend

- deposit received

- transfer executed

5) Do one monthly review

Once a month, ask:

- Did the spend account hit zero too early?

- Did I move money back from savings? Why?

- What is one adjustment for next month?

Sources and further reading

- Heath, Chip and Jack B. Soll (1996). Mental Budgeting and Consumer Decisions. Journal of Consumer Research, 23(1), 40–52. Budgets as self-control; spending changes when a budget feels depleted.

- Soman, Dilip and Amar Cheema (2011). Earmarking and Partitioning. Journal of Marketing Research, 48(SPL), S14–S22. Partitioning savings into separate containers can increase saving.

- Thaler, Richard H. and Shlomo Benartzi (2004). Save More Tomorrow. Journal of Political Economy, 112(S1), S164–S187. Pre-commitment + automation can raise saving rates over time.

- Ashraf, Nava, Dean Karlan and Wesley Yin (2006). Tying Odysseus to the Mast. Quarterly Journal of Economics, 121(2), 635–672. Commitment features and restricted access can increase accumulation.

- Loewenstein, Cryder, Benartzi and Previtero (2012). Addition by Division: Partitioning Real Accounts for Financial Well-Being. Partitioning “real” accounts can support self-control and well-being.

- Experian — How to Budget Using Multiple Accounts. A mainstream mechanics overview, for comparison.

If you have been trying to “just be disciplined,” try the system instead. Set the transfer, separate the money, and let your brain relax inside clear boundaries.

Keep reading

Vibe-Coding a Real Revenue Product: Where It Works and Where It Breaks in 2026

I shipped a $29/month niche SaaS in eleven weeks using Cursor and Claude Sonnet — here is the honest post-mortem...

Build in Public ROI: Does Transparency Actually Drive MRR? (2026 Data)

An evidence-based audit of build-in-public strategy using 2025–2026 data from 20 indie hackers — revealing that BIP only drives measurable...

Lean vs Fat FI Target for the Founder Who Can Always Earn More

A founder with marketable skills has a different FI risk profile than a salaried retiree — here is how to...

Section 179, Vehicle & Home-Office Deductions Done Right: The Audit-Safe Founder Playbook

Section 179 and home-office deductions can save founders thousands — but the vehicle caps, business-use rules, and S-corp accountable plan...

Boring Business Second Income Stream: De-Risk Your Startup with Predictable Cash

A boring business—vending route, cleaning company, or laundromat—can generate $2k–$4k/month in predictable net income that makes a startup's zero-revenue phase...

Broker vs. Direct Sale: Fees, Outcomes, and When Each Path Wins for Founders

Business brokers charge 8–12% on sub-$1M deals — on a $1M exit that's up to $120K off the top. This...

You've reached the end — no more posts to load.

No comments yet — be the first to share your thoughts.