FIRE Travel Paradox: Travel More, Spend Less (2026)

Travel before FIRE without wrecking your savings rate: a hard travel cap plus shoulder-season timing, booking-day edges, and slow travel. Sourced numbers.

FIRE travel can feel like a contradiction: travel matters to you, but travel spending slows compounding. The usual advice is to delay the fun until the number is hit. The paradox is that many FIRE pursuers can travel earlier and spend less overall by designing trips around a few repeatable levers instead of deprivation.

In this post you’ll build a rules-based travel system that fits your FIRE math, then use timing and simple trip-design choices to get more travel per dollar — without going into debt or hating the trip.

Quick summary — the 5 levers:

- Sinking fund + cap: a dedicated travel fund and annual limit so travel does not leak into your savings rate

- Shoulder season timing: often the biggest price lever, without cutting the experience (varies by route and weeks)

- Flight comparisons: small probability edges from day-of-week comparisons, alerts, and flexibility

- Slow travel: fewer hops, longer stays, lower daily spend and less stress

- Optional points: only if you already pay in full (and treat points as a discount, not a plan)

The FIRE travel paradox: why delaying travel often backfires

FIRE logic is clean: spend less now, invest the difference, let compounding do the heavy lifting. But travel is different from a lot of other “fun” spending because it is time-sensitive. A decade from now you might have more money, but you might have less flexibility, different responsibilities, or less appetite for the kind of travel you want.

There is also a quieter bottleneck: many people are not using the vacation time they already have. SHRM reported that 48% of U.S. workers said they did not expect to take all of their allotted vacation days by the end of the year (published December 2024). That does not mean everyone can travel more. It does suggest that, for a big chunk of people, “more travel” starts with intentional planning and norms — not only money.

The goal here is not uncontrolled spending, and not “travel hacking” your way out of reality. We are designing travel inside a plan with a hard cap, then using levers that reduce cost without reducing joy. (If travel envy from your feed is part of the pressure, read why social media might be hurting your FIRE dreams first.)

Rule zero: travel only if it fits your FIRE math (no debt, no vibes)

Before tactics, you need constraints. Without rules, travel becomes a budget leak that feels justified because it is “meaningful.”

The core rule: travel happens only from a dedicated travel sinking fund, inside an annual cap, and never with consumer debt.

A setup that works:

- Create a separate travel account (or budget category).

- Fund it automatically each paycheck.

- Set an annual travel cap that your FIRE plan can absorb.

Cap options:

- Percent cap: an example range is 2%–5% of take-home pay, only if it still preserves your target savings rate and FI timeline.

- Fixed cap: a flat annual number already baked into your FI timeline.

- Trip cap: a maximum per trip (useful if you travel irregularly).

If your plan assumptions break, you do not “wing it.” You adjust travel design: timing, destination proximity, trip length, or number of hops.

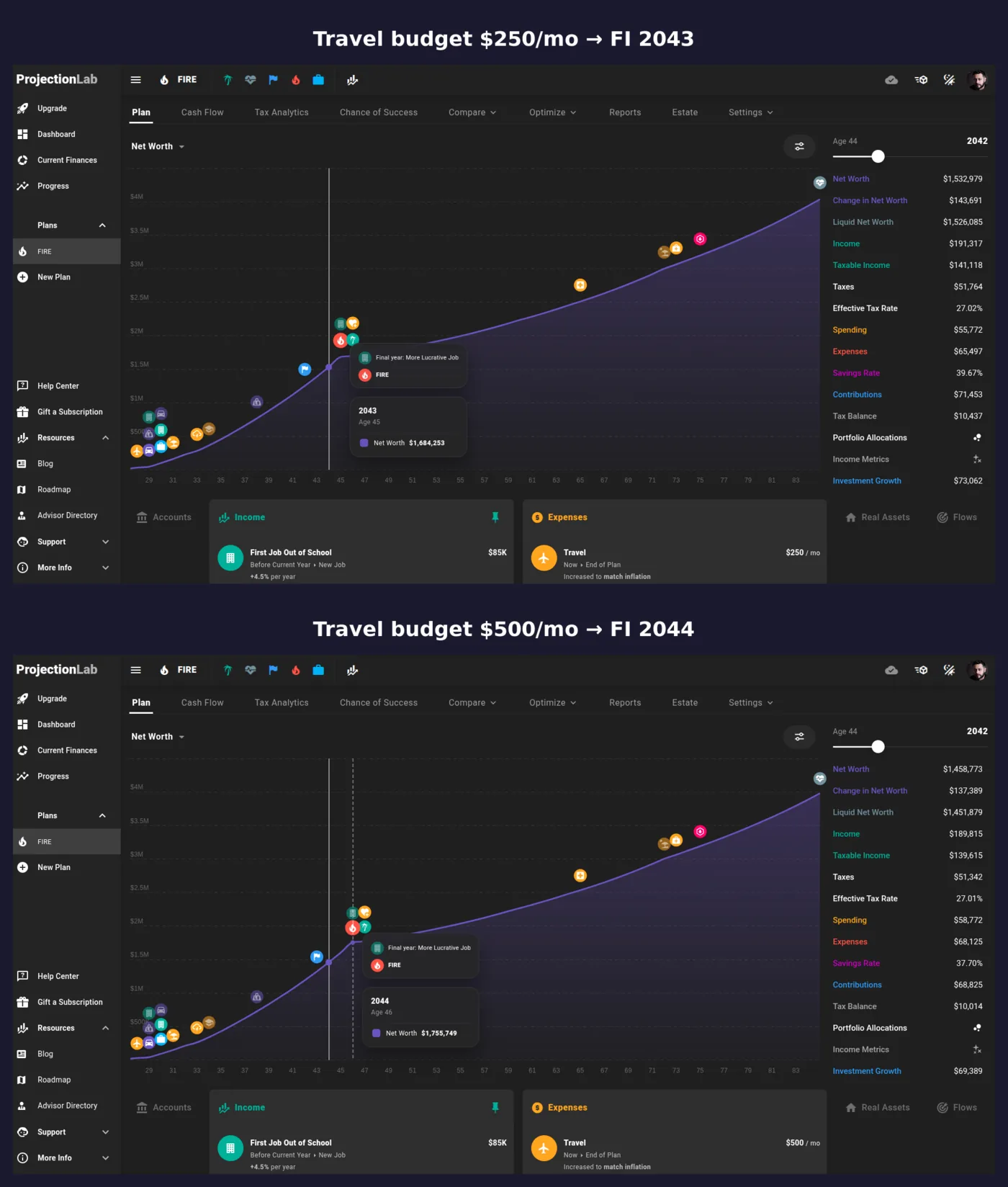

We ran this exact comparison in ProjectionLab’s sandbox: with a $250/month travel budget the plan reaches FI in 2043 at age 45 (39.67% savings rate); bumping the budget to $500/month pushes FI to 2044, age 46 (37.70% savings rate). Doubling the travel line cost about a year of working life in this scenario — a real price, but a visible one you can choose deliberately instead of discovering later.

Lever 1: timing beats frugality — use shoulder season to buy the same trip cheaper

Most people try to save money on travel by shrinking the experience: worse lodging, fewer activities, constant stress. The biggest lever is usually simpler: shift when you go.

KAYAK’s shoulder-season analysis highlights that prices can be meaningfully lower outside peak summer, including examples like international airfare down about 33% and domestic airfare down about 21% in their reporting. Clarifying scope: KAYAK’s analysis compares peak-summer weeks vs shoulder-season weeks in their dataset, and the results are not universal — they vary by route, destination, and the specific weeks you compare.

Why shoulder season is so powerful:

- You often get lower prices without cutting quality

- Crowds tend to be lighter

- The same destinations can feel more enjoyable

The tradeoffs:

- Weather is sometimes less predictable

- Some attractions have shorter hours

- Families tied to school schedules have fewer options

How to validate shoulder season for your exact trip (2 minutes before you commit):

- Open your flight tool (Google Flights, airline site, etc.).

- Compare 2–3 adjacent weeks: your most likely peak-week dates vs one shoulder-season week nearby.

- Keep everything else identical (same airports if possible).

- If the shoulder week is not meaningfully cheaper, do not force it — use the other levers below.

Lever 2: tiny rules that compound — booking day and fly-day choices

After timing, the next-best lever is smaller edges that can add up over multiple trips. This is a system, not a hack: use fare alerts and reasonable booking windows first, then test day-of-week as a secondary lever.

Expedia’s 2025 Air Hacks report says Sunday is the cheapest day to book on average, and cites potential savings of about 6% for domestic travel and about 17% for international travel compared to booking on a Monday or Friday. Treat it as dataset-based guidance that can vary by route, season, and demand.

Expedia also highlights that departure day can change prices, calling out Thursday and Saturday as lower-cost departure options in their dataset. Use this as a prompt to compare departure days rather than as a fixed rule.

A simple ruleset that is easy to repeat:

- Start with fare alerts and a booking window that fits your trip (day-of-week is a smaller lever than timing and alerts).

- When you are within your decision window, test booking day (including Sunday) as a quick comparison.

- If you have flexibility, compare departure days directly (try Thu and Sat against Sun).

How to validate for your trip (so you are not trusting averages): pick your exact route and dates, then run three checks — different departure days, different return days, and the same trip 1–2 weeks earlier or later. Screenshot the best 2–3 options, then decide on total cost and convenience.

Lever 3: slow travel — fewer hops, longer stays, lower daily spend

“Travel more” fails when travel becomes exhausting. Packing, airports, check-ins, constant movement. It burns energy and money.

Slow travel is the opposite: fewer hops, longer stays, one base.

Why it helps your budget:

- Less transportation churn (fewer flights, trains, taxis, transfers)

- Fewer repeated fixed costs (bags, local transit spikes, last-minute logistics)

- Cheaper routines emerge naturally (groceries, local cafes, free parks)

Why it helps happiness:

- Less time spent on logistics

- More time actually living in the place

- Short PTO stretches feel bigger. Example: 4 days off can become 6 nights in one base if you pair weekends with one midweek flight.

Lever 4: the budget cap that keeps you sane — a simple travel system

A travel budget that is only about cutting costs tends to produce miserable trips. A travel budget that is only about “making memories” tends to blow up your FIRE plan. The solution is a system with caps and non-negotiables — the same logic that separates habits that move the math from habits that just sound smart.

Step 1: Choose your cap structure

- Annual cap (best for planning)

- Per-trip cap (best for occasional travel)

- Percent cap (best if income fluctuates)

Step 2: Use a 3-bucket trip budget

- Transport

- Lodging

- Experiences

Step 3: Pre-commit your happiness spending (before the trip). Examples of non-negotiables:

- Pay for a location that reduces rides and saves time.

- Pick one paid highlight experience, keep the rest low-cost.

- Eat out once per day, groceries the rest.

The point is not to spend the least. The point is to spend predictably on what you value, inside your cap.

Points basics: treat rewards as optional discounts, not free travel

Rewards can be useful, but they are not magic. They can backfire if they increase spending or create debt.

The conservative rule: points are optional optimization, only if you already pay in full every month.

Keep expectations realistic:

- Programs change and points can be devalued.

- Award availability can be limited.

- Annual fees and redemption fees can erase the benefit if you do not use the card intentionally.

A safe way to use points: use a travel card only if it fits your existing spend, auto-pay the statement balance in full, and treat points as a rebate, not a reason to buy. NerdWallet’s FIRE-and-travel guidance lands in the same place: protect the savings rate first, optimize second.

A worked example: realistic ranges using an airfare benchmark

This section is about budgeting, not guarantees.

BTS reported the average U.S. domestic itinerary airfare as $397 for Q1 2025. Use this as a planning anchor, not a quote for your specific route.

Say you want two domestic trips this year. Baseline airfare budget: 2 × $397 = $794.

Now compare each lever as a separate scenario. Some of these overlap; treat the stack as directional, not promised.

Scenario A: Timing (shoulder season vs peak)

- Worst case: no meaningful difference on your route (still near $397).

- Base case: modest improvement if shoulder dates price lower.

- Best case: KAYAK’s reporting shows examples like domestic airfare around 21% lower in shoulder season vs peak summer (varies by route and weeks).

Scenario B: Departure day

- Worst case: no meaningful difference on your route.

- Base case: small improvement by avoiding the priciest day.

- Best case: Expedia’s dataset shows Thursday and Saturday departures often pricing below higher-demand days. If you can move by 1 day, you might unlock savings without changing the trip.

Scenario C: Booking day

- Worst case: no meaningful difference.

- Base case: a small average edge.

- Best case: Expedia cites about 6% domestic and about 17% international savings booking Sunday vs Monday/Friday (dataset-based, not guaranteed).

The FIRE-friendly framing: you do not assume savings in advance. You run the quick comparisons, lock in the best option that still fits your schedule, and then either reinvest the savings (see pay off debt or invest?) or redeploy them into an extra micro-trip, within your cap.

Constraints and honest caveats

Some people cannot travel more often because they do not have time. In the U.S., paid vacation is not federally required; vacation benefits depend on employers. The U.S. is unusual among rich countries in not requiring paid vacation, which makes time constraints a real limiter for many people.

School calendars, caregiving constraints, and rigid jobs are real. That is why this approach uses multiple levers. If shoulder season is impossible:

- Compare departure days and return days

- Use nearby airports

- Choose closer destinations

- Use slow travel to reduce churn and daily costs

The thesis is not “everyone can travel more.” The thesis is: if you can travel at all, you can often travel earlier and spend less by designing smarter, not suffering harder.

Sources and further reading

- KAYAK — How shoulder season travel stacks up. Peak-summer weeks vs shoulder-season weeks in KAYAK’s dataset, with reported deltas for airfare, hotels, and rental cars.

- Expedia — 2025 Air Hacks Report. Dataset-based analysis of airfare patterns by booking day and departure day.

- U.S. Bureau of Transportation Statistics — Q1 2025 average air fare. Average U.S. domestic itinerary airfare: $397.

- SHRM — Nearly half of employees expect to leave vacation time unused (December 2024).

- U.S. Department of Labor — Vacation Leave. Paid vacation is not federally required in the U.S.

- NerdWallet — Financial Independence + Travel: 3 Savvy Tips.

Keep reading

Vibe-Coding a Real Revenue Product: Where It Works and Where It Breaks in 2026

I shipped a $29/month niche SaaS in eleven weeks using Cursor and Claude Sonnet — here is the honest post-mortem...

Build in Public ROI: Does Transparency Actually Drive MRR? (2026 Data)

An evidence-based audit of build-in-public strategy using 2025–2026 data from 20 indie hackers — revealing that BIP only drives measurable...

Lean vs Fat FI Target for the Founder Who Can Always Earn More

A founder with marketable skills has a different FI risk profile than a salaried retiree — here is how to...

Section 179, Vehicle & Home-Office Deductions Done Right: The Audit-Safe Founder Playbook

Section 179 and home-office deductions can save founders thousands — but the vehicle caps, business-use rules, and S-corp accountable plan...

Boring Business Second Income Stream: De-Risk Your Startup with Predictable Cash

A boring business—vending route, cleaning company, or laundromat—can generate $2k–$4k/month in predictable net income that makes a startup's zero-revenue phase...

Broker vs. Direct Sale: Fees, Outcomes, and When Each Path Wins for Founders

Business brokers charge 8–12% on sub-$1M deals — on a $1M exit that's up to $120K off the top. This...

You've reached the end — no more posts to load.

No comments yet — be the first to share your thoughts.