Why Tracking Every Expense Makes You Worse With Money

Tracking every expense often backfires: more stress, worse decisions. Here is the behavioral science — and the automation-first system to use instead.

The Popular Advice That Sounds Responsible

If you have ever searched for money advice, you have heard the same recommendation over and over: track every expense. Write down every coffee, every subscription, every small purchase. The logic sounds airtight — if you know where your money is going, you can control it.

For some people, logging expenses feels empowering at first. It creates a sense of order. It feels like finally being an adult with money.

But for many people — especially anyone who already feels anxious about finances, or anyone with irregular income — this well-meaning advice quietly makes things worse. Even YNAB, a company that sells budgeting software, draws a hard line here: expense tracking is not budgeting. Recording what already happened is autopsy, not strategy.

Why Tracking Every Expense Creates Stress

Tracking every expense turns money into a constant background task. Every purchase becomes a decision that needs to be recorded, categorized, and judged. That does not just take time. It takes mental energy.

Behavioral research backs this up. In a series of studies published in Science, Sendhil Mullainathan and colleagues showed that preoccupation with scarce resources consumes cognitive bandwidth — people primed to worry about money performed measurably worse on reasoning tasks. A system that forces you to think about money dozens of times a day is a system that taxes the exact mental capacity you need for good decisions.

Small deviations from the plan start to feel like personal failures. A spontaneous meal or an unexpected cost does not just affect your budget — it affects your mood. Over time, money stops being a tool and starts feeling like a scoreboard you are losing.

What Behavioral Finance Reveals

Humans do not naturally think in precise line items. We think in broad categories. Forcing yourself to track every dollar fights how your brain prefers to manage complexity. Instead of clarity, you get friction.

Worse, self-control strategies that require constant monitoring are fragile by design: they work when life is calm and break down when stress increases. Stress is exactly when you need your financial system to hold. This is the same reason most habits collapse after the first month — they depend on daily willpower instead of structure.

Even advisors who recommend awareness concede the point. Thrive Wealth Management’s position is representative: you need to know your big numbers, not where every dollar goes.

Why Most People Quit Tracking

Quitting is not a personal failure. It is a predictable outcome of a system with a daily maintenance cost.

Expense tracking relies on continuous effort and attention. Miss a few days and the system feels broken. Catching up feels overwhelming. Eventually the app gets opened less and less, and the quitter feels worse than when they started — now they have failed at budgeting, too.

The problem is not discipline. The problem is design.

When Expense Tracking Actually Helps

Tracking is not useless. It works as a diagnostic, not a lifestyle:

- A 30–60 day audit to discover your real baseline spending — once, or once a year.

- A targeted spotlight on one leaky category (eating out, software subscriptions) for a few weeks.

- A short runway check before a major change: quitting a job, starting a business, moving abroad.

Founders should treat their business the same way: a periodic subscription audit beats logging every invoice forever.

A Better Way to Manage Money: Automate the Decisions

The alternative is not ignoring your finances. It is shifting from attention-based systems to automation-based systems:

- Pay yourself first. An automatic transfer to savings/investments on payday, before anything else can spend it.

- Automate fixed bills. Rent, utilities, insurance — decided once, executed silently.

- Give yourself a spending boundary, not a ledger. Whatever is left after savings and bills is genuinely spendable, no itemized guilt required.

Decide in advance what happens to your money so you do not have to re-decide it every day. When the system runs in the background, your mental energy is freed for decisions that actually move the math — like whether to pay off debt or invest, or which money habits actually matter versus just sounding smart.

The Founder Wrinkle: Irregular Income Makes Tracking Even Worse

If your income is a paycheck, tracking is merely tedious. If your income is a business — lumpy months, annual contracts, seasonal swings — per-expense tracking produces noise, not signal. A $4,000 month followed by a $15,000 month makes every category comparison meaningless.

The fix is percentage-based automation: a fixed percentage of every deposit routes to taxes, savings, and investing the day it lands. The system flexes with income while the structure stays constant. This matters double for founders, because your income stream already carries sequence risk — your financial system should absorb volatility, not amplify it.

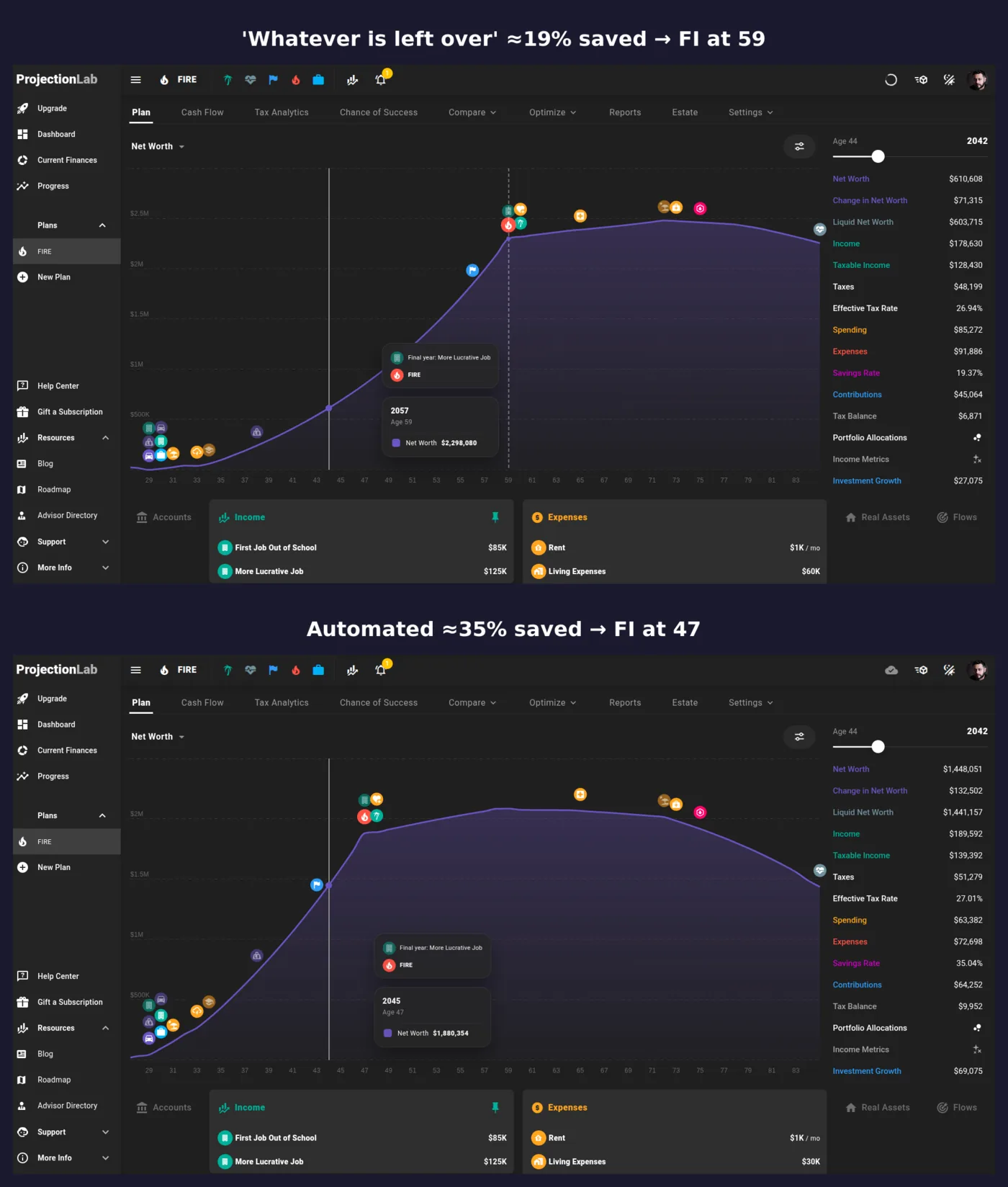

We ran both trajectories in ProjectionLab’s sandbox with the same income: a “save whatever is left over” pattern that works out to about a 19% savings rate reaches FI at age 59, while an automated transfer locking in roughly 35% reaches FI at age 47 (2045). Twelve years of difference — and none of it comes from watching expenses more closely.

For many people, doing less with money — fewer daily decisions, more pre-made ones — is exactly what leads to better results.

Keep reading

The FIRE Two-Account Trick: Spend Guilt-Free, Save More

Separate spend from save and saving becomes the default. The peer-reviewed science behind the two-account trick, plus the 4 failure...

FIRE Decision Tree: Buy vs Rent vs Relocate in 5 Minutes

Buy, rent, or relocate? Run this FIRE decision tree in 5 minutes: tenure buckets, mortgage rate, transaction frictions — decided...

FIRE Stress Test: Will Your Plan Survive a Bad Decade?

Most FIRE plans assume average years. This 10-question stress test finds your weak spot — sequence risk, inflation, job loss...

Recession as Opportunity: How to Acquire a Cash-Flowing Business When Everyone Else Is Scared

Most people sit on the sidelines during a downturn. Operators with capital and a clear thesis use recessions to acquire...

Churn Math: How 5% vs 3% Monthly Churn Reshapes Your FI Timeline

A data-driven cohort analysis showing how monthly churn rate at 5%, 3%, and 1.5% reshapes MRR trajectory, LTV, and your...

The One-Person Company Playbook: AI Automations That Run Your Business While You Sleep

A full-stack founder's architecture for one person company AI automation: five n8n workflow layers covering lead capture, onboarding, support triage,...

You've reached the end — no more posts to load.

No comments yet — be the first to share your thoughts.